RELAXATIONS UNDER INCOME TAX ACT

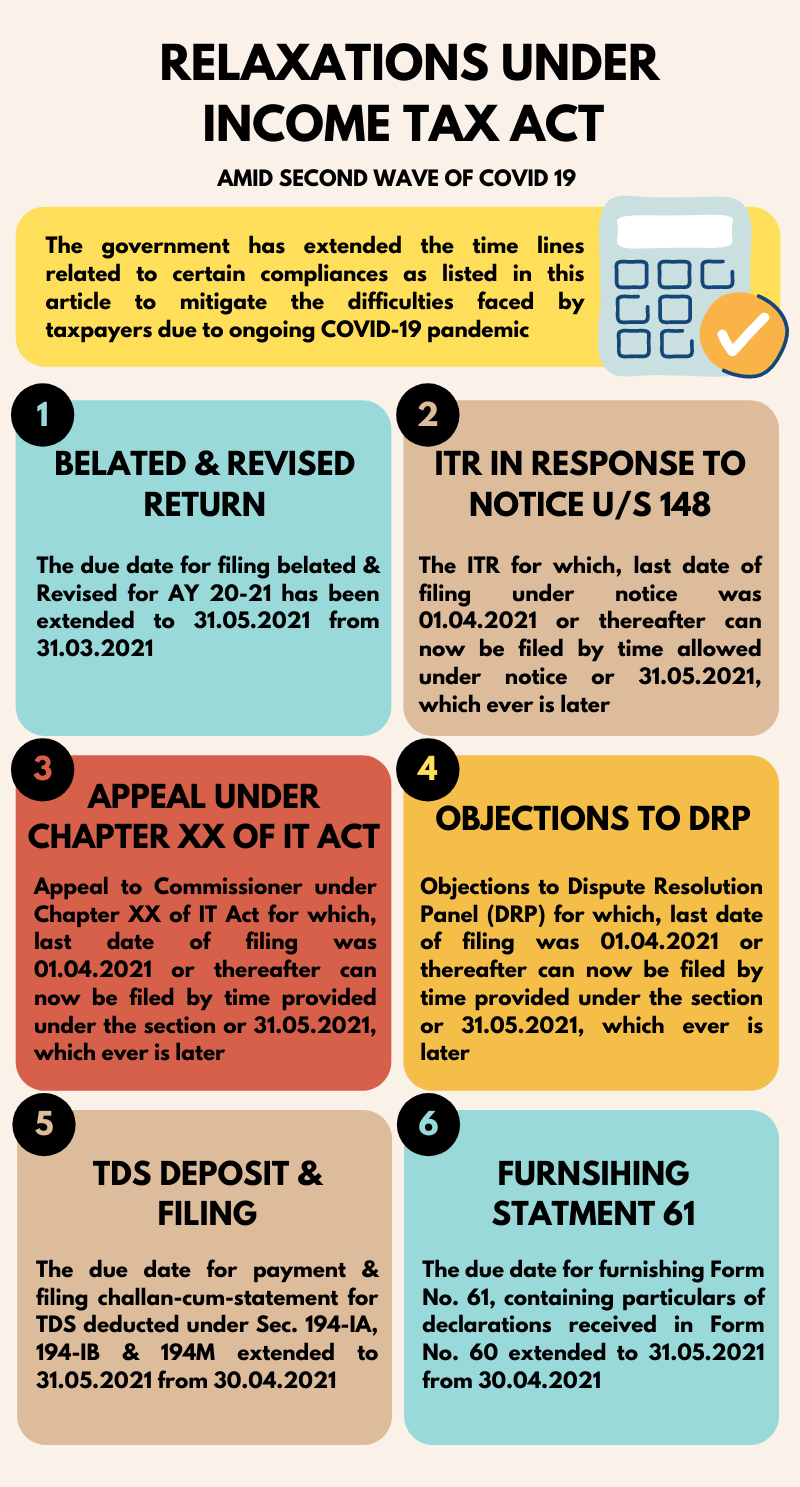

In view of severe pandemic, the government provides following relaxation in respect of Income-tax compliances by the taxpayers: -

a) BELATED & REVISED RETURN – Filing of belated return and revised return for Assessment Year 2020-21, which was earlier required to be filed on or before 31st March 2021, can now be filed on or before 31st May 2021.

b) ITR IN RESPONSE TO NOTICE U/S 148 – Income-tax return in response to notice under Section 148 of the Income-tax Act, for which the last date of filing of return of income under the notice was 1st April 2021 or thereafter, can now be filed within the time allowed under that notice or by 31st May 2021, whichever is later.

c) APPEAL UNDERCHAPTER XX OF IT ACT – Appeal to Commissioner (Appeals) under Chapter XX of the Income-tax Act, for which the last date of filing under the Section was 1st April 2021 or thereafter, can now be filed within the time provided under the Section or by 31st May 2021, whichever is later.

d) OBJECTIONS TO DRP – Objections to Dispute Resolution Panel (DRP) under Section 144C of the Income-tax Act, for which the last date of filing under the Section was 1st April 2021 or thereafter, can now be filed within the time provided under that Section or by 31st May 2021, whichever is later.

e) TDS DEPOSIT & FILING – Payment and filing of challan-cum-statement for tax deducted under Section 194-IA, Section 194-IB and Section 194M of the Income-tax Act, which are required to be paid and furnished by 30th April 2021, can now be paid, and furnished on or before 31st May 2021.

f) FURNSIHING STATMENT 61 – Statement in Form No. 61, containing particulars of declarations received in Form No.60, which was due to be furnished on or before 30th April 2021, can now be furnished on or before 31st May 2021.

Disclaimer:“Information contained herein is for informational purposes only and should not be used in deciding any particular case. The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Though utmost efforts have been made to provide authentic information, it is suggested that to have better understanding and obtaining professional advice after thorough examination of particular situation.”

Please share:

Prepared By

Sujeet Patro

Articled Assistant

Date: 11-06-2021