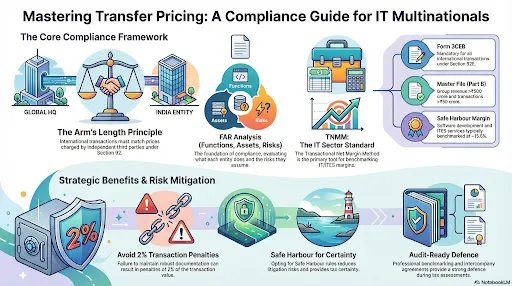

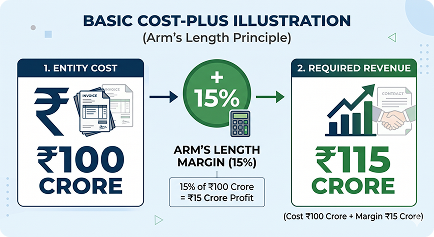

1. What is transfer pricing?

It is pricing of transactions between related entities across borders, governed by Section 92.

2. Who needs transfer pricing compliance?

Entities entering into international transactions under Section 92B, especially multinational IT companies.

3. What documents are required?

As per Section 171 & Rule 123

- FAR analysis

- Benchmarking study

- Financial analysis

- Agreements

- Form 3CEB

4. What are penalties?

Sections 442 / 457

- 2% of the transaction value for not maintaining documentation

- ₹1,00,000 (failure to file Form 48)

- Additional penalties for misreporting

5. How can experts help?

Experts:

- Perform accurate FAR & margin analysis

- Ensure Safe Harbour optimisation

- Defend during audits

- Align TP with global strategy