New Composition Scheme under GST

Compliance is something that can add to the woes of a business and which may sometimes affect the profitability as well. The businessmen of the country have to be compliant in respect of various laws and regulations under the various Acts framed by the lawmakers, like the Income Tax, Goods and Service Tax, Customs etc… With India aiming to jump higher in the rank of Ease of doing Business, the composition of scheme under GST might just aid in the same.

Vide Notification No. 2/2019-Central Tax (Rate) dated 7th March 2019, the council notified the new composition scheme. Let’s have a quick glance at what this scheme has to offer for us

Purpose of the scheme

The earlier composition scheme under GST was limited only to traders and Restaurants not serving alcohol. So if a GST Registered service provider had mere turnover of Rs 25 Lakhs, he has to file GSTR1, GSTR 3B, GSTR 9 amounting to a minimum of 17 returns per year.

In order to provide relaxation for the service providers as well, the council has come up with the new composition scheme. This scheme has come into effect from 01st April 2019.

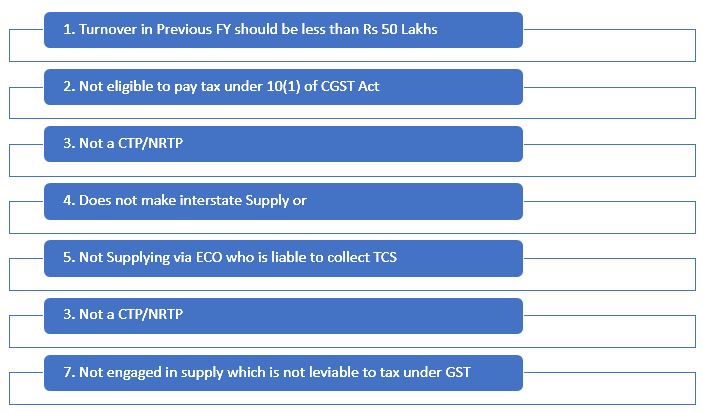

Eligibility for the new Composition scheme

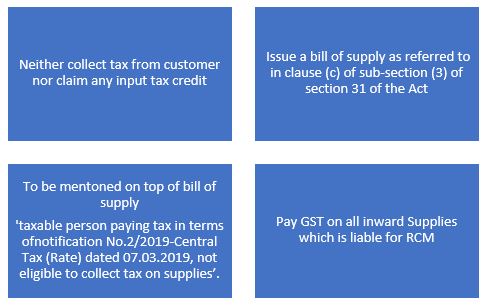

Things to be taken care of

Even under the composition scheme, there are some minimal things which are to be taken care of.

In case of multiple Registrations

Where there are multiple registrations under a single PAN, then if one registered person opts for composition scheme, then all the registered persons must also opt for the composition scheme under the same PAN.

Eg: if total turnover under one PAN is Rs 60 Lakhs and it has 6 registered GSTIN each of whose turnover is Rs.10 Lakhs. If they want to opt for the new composition scheme, then all 6 GSTIN should opt for Composition scheme

If total Turnover of a PAN is Rs 55 Lakhs and it has 3 GSTIN registered under it out of which turnover of 1 GSTIN is 51 Lakhs and other 2 GSTIN is Rs 2 Lakhs each then none of them can opt for Composition scheme.

Dealer of Specified Goods not eligible for Composition scheme

Dealers of the below mentioned items are not eligible to opt for the below Composition scheme.

| Sl No. | Tariff item, subheading, heading or Chapter | Description |

|---|---|---|

| 1 | 2015 00 00 | Ice cream and other edible ice, whether or not containing cocoa |

| 2 | 201 90 20 | Pan Masala |

| 3 | 24 | Tobacco and Manufactured Tobacco Substitutes |

Impact on IT&ITeS Industry

India is now a Hub for upcoming IT Startups and we see numerous startups taking birth every day.

In our opinion, the composition scheme is not advisable to for any entity dealing with IT and ITeS industry unless they are operating very small scale and wherein composition scheme tends to be more convenient and profitable for them.

Also such entities would like to expand their market apart from their place of business and may deal into inter state supply. Therefore, they would not be eligible to opt for this scheme.

But In general, it is better to have a regular registration, as under the composition scheme we pay the tax from our pocket. But whereas under regular scheme we can collect the GST from our customers and remit the same

Ideally, if a business has more inputs from a registered supplier, it is generally not advisable to take up the composition scheme, as they would miss out on those inputs and the RCM inputs if any. However, small taxpayers with considerably less inputs may opt for the composition scheme.

It is clearly evident that the government wants the small businesses to flourish with much lesser compliances for which schemes such as this are brought in.

B C Shetty and Co. can aid you in deciding as to whether to opt for composition scheme or not and also assist you in being compliant in respect of the same.

Disclaimer:“The information contained herein is only for informational purpose and should not be considered for any particular instance or individual or entity. We have obtained information from publicly available sources, there can be no guarantee that such information is accurate as of the date it is received or it will continue to be accurate in future. No one should act on such information without obtaining professional advice after thorough examination of particular situation.”

Please share:

Prepared By

Srivatsa Jois H S

Article Assistant

Date:02/06/2020